3Y

...

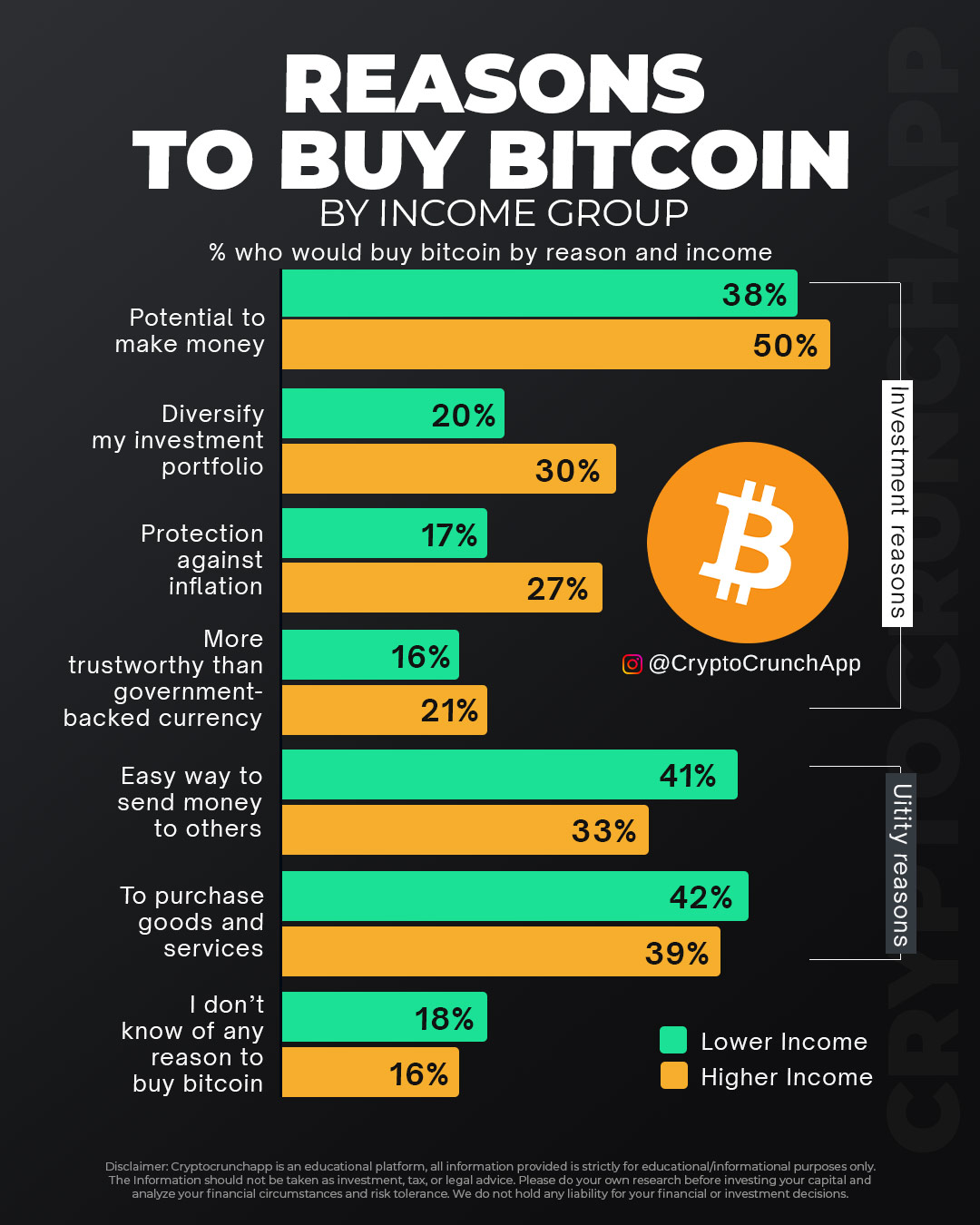

When it comes to investing in Bitcoin, it appears that motivations can vary significantly depending on one’s income level. A deeper look into the reasons why individuals from different income brackets consider purchasing Bitcoin reveals interesting patterns that highlight the diverse appeal of this cryptocurrency.

For those with higher incomes, the primary lure seems to be the potential for Bitcoin to generate profits, with 50% citing the possibility of making money as a key reason for investment. This could be indicative of a greater propensity for risk-taking and investment in speculative assets among individuals who are financially more secure.

On the other hand, the drive to diversify investment portfolios with Bitcoin is more evenly spread across income levels, though still more prevalent among the higher income group at 30% compared to 20% in the lower income bracket. This suggests that while portfolio diversification is a common investment strategy, those with higher incomes might have more capital to allocate to diverse asset classes, including cryptocurrencies.

Protection against inflation is another reason that resonates more with the higher income group. With 27% of higher earners viewing Bitcoin as a hedge against inflation, it underscores a strategic approach to preserving purchasing power in the face of currency devaluation—a concern that might be more pressing for those with significant capital to protect.

The concept of trust in currency plays an interesting role, with a notable portion of lower-income respondents, 21%, considering Bitcoin more trustworthy than government-backed currencies. This could reflect a skepticism of traditional financial institutions or a response to economic conditions where conventional currencies have failed to retain value.

Utility reasons for buying Bitcoin, such as the ease of sending money to others and purchasing goods and services, are more favored by the lower income group. This could indicate that for them, Bitcoin is not just an investment but also a functional currency that addresses certain needs or inefficiencies in the current financial systems.

Interestingly, a segment of the population remains unconvinced about Bitcoin’s merits, with 18% of the lower income group and 16% of the higher income group not recognizing any reason to buy Bitcoin. This skepticism or lack of information could represent an opportunity for educational initiatives to bridge the gap in understanding the potential benefits and risks of cryptocurrency investments.

The analysis of these investment reasons reveals a complex tapestry of financial motivations and behaviors. It highlights how socioeconomic factors can influence one’s approach to new investment vehicles like Bitcoin. With such a diverse array of incentives at play, it becomes clear that the narrative around Bitcoin is not one-size-fits-all but rather a reflection of individual financial goals and the economic landscape each investor navigates.